The Pros and Cons of CDs (Certificates of Deposit)

Certificates of deposit have a reputation as an old-fashioned, low-excitement savings tool — and in some ways that’s accurate, but it’s also exactly what makes them useful for specific savings goals where stability matters more than flexibility or maximum growth.

What a CD Actually Is

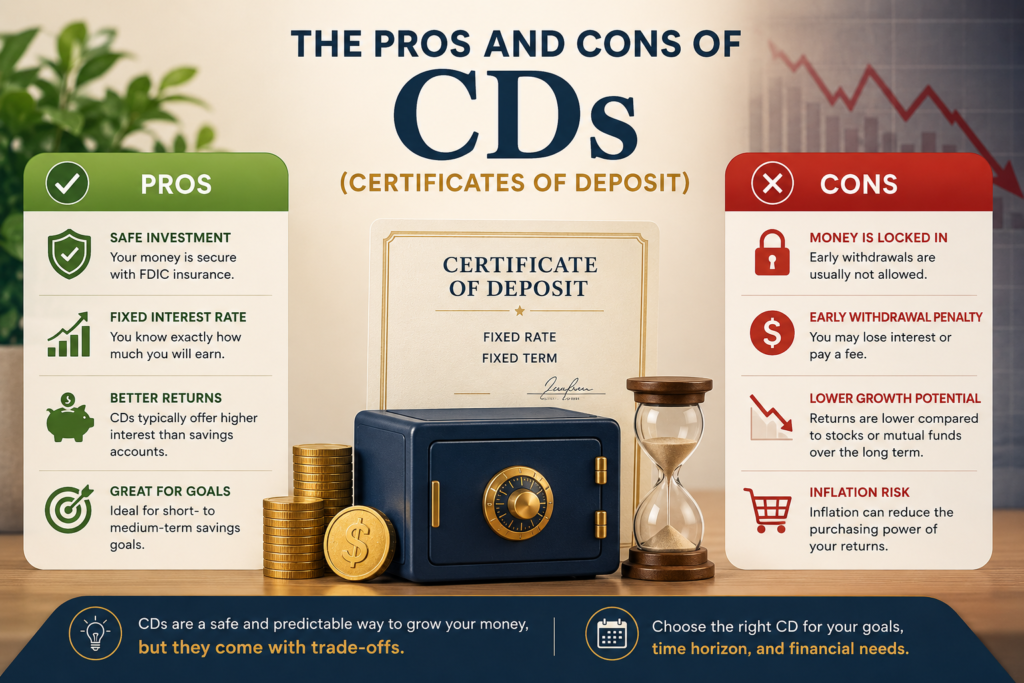

A certificate of deposit is a savings product where you agree to deposit a fixed amount of money for a set term — commonly ranging from a few months to five years or more — in exchange for a fixed interest rate that’s typically higher than a standard savings account. The tradeoff is reduced access: withdrawing the money before the term ends usually triggers an early withdrawal penalty.

The Core Appeal: A Locked-In, Predictable Rate

Unlike a high-yield savings account, where the interest rate can change at any time based on broader market conditions, a CD’s rate is fixed for the entire term once you open it. This predictability is the central value proposition — you know exactly what you’ll earn, regardless of what happens to interest rates during the term.

The Core Tradeoff: Reduced Liquidity

The primary downside of a CD is that your money isn’t easily accessible without a penalty until the term ends (the “maturity date”). Early withdrawal penalties vary by institution and term length but commonly involve forfeiting some amount of the interest earned, sometimes more for longer-term CDs withdrawn early. This makes CDs unsuitable for money you might need access to on short notice, including most emergency funds.

Comparing CDs to Other Savings Options

| Feature | High-Yield Savings | CD |

|---|---|---|

| Rate type | Variable, can change anytime | Fixed for the term |

| Access to funds | Fully liquid, no penalty | Locked until maturity, penalty for early withdrawal |

| Best for | Emergency funds, flexible short-term goals | Money you won’t need until a known future date |

| FDIC insured | Yes (at insured institutions) | Yes (at insured institutions) |

When a CD Makes Sense

- You have a specific savings goal with a known timeline — for example, money set aside for a down payment you won’t need for 18 months, matching a CD term of similar length.

- You want to lock in a favorable rate before an anticipated decline in interest rates, securing predictable earnings regardless of future rate changes.

- You’re confident you won’t need the funds before maturity, since the money already has a clear purpose and timeline that doesn’t require flexible access.

- You want a safer alternative to investing for money you don’t want exposed to stock market volatility but also don’t need immediate access to.

When a CD Doesn’t Make Sense

- For an emergency fund, which by definition needs to be accessible without penalty or delay when an actual emergency occurs.

- If you’re unsure when you’ll need the money, since locking in a term you might need to break early generally costs more in penalties than the benefit gained from the fixed rate.

- If current CD rates aren’t meaningfully better than a high-yield savings account, in which case the reduced flexibility isn’t compensated by a meaningfully better return.

CD Laddering: Balancing Rate Lock-In With Some Flexibility

A CD ladder involves splitting savings across multiple CDs with staggered maturity dates rather than putting everything into one CD with one term. For example, instead of a single $12,000 CD locked for three years, you might open four CDs of $3,000 each with terms of 6, 12, 18, and 24 months. As each CD matures, you can either access that portion of the money or reinvest it into a new CD, creating a rolling structure that provides periodic access points while still benefiting from CD rates on the bulk of the savings.

| CD | Amount | Term | Matures |

|---|---|---|---|

| CD 1 | $3,000 | 6 months | Month 6 |

| CD 2 | $3,000 | 12 months | Month 12 |

| CD 3 | $3,000 | 18 months | Month 18 |

| CD 4 | $3,000 | 24 months | Month 24 |

What Happens at Maturity

When a CD reaches its maturity date, you typically have a short window (often 7-10 days, though this varies by institution) to decide whether to withdraw the funds, move them elsewhere, or let the CD automatically renew into a new term at the prevailing rate. Missing this window often results in automatic renewal, sometimes at a rate less favorable than what’s currently available elsewhere, so marking maturity dates and reviewing your options in advance is a worthwhile habit.

Frequently Asked Questions

Are CDs a good place for retirement savings?

Generally not as a primary retirement savings vehicle for younger savers with a long time horizon, since CDs typically offer lower long-term returns than diversified stock market investing over many decades. CDs can play a role for retirees or those nearing retirement who want a portion of savings in a stable, predictable vehicle, but this is a decision worth discussing with a financial advisor given individual circumstances.

What happens if I need to withdraw from a CD early due to an emergency?

You generally can withdraw early, but you’ll typically forfeit some portion of the interest earned as a penalty, and in rare cases with very short-term CDs, you could potentially receive slightly less than your original deposit if the penalty exceeds interest earned. This is exactly why CDs aren’t recommended for true emergency funds.

Is a CD better than just leaving money in a high-yield savings account?

This depends on current rate differences and your need for access to the funds. When CD rates are notably higher than high-yield savings rates and you’re confident about the timeline, a CD can make sense; when rates are similar or you need flexibility, a high-yield savings account is usually the more practical choice.

Are all CDs FDIC insured?

CDs from FDIC-member banks are insured up to standard limits, same as other deposit accounts, and credit union CDs are typically insured similarly through NCUA. It’s worth confirming this directly for any specific institution before depositing funds, since not all financial products marketed similarly to CDs carry the same insurance protections.

The Bottom Line

CDs aren’t designed to compete with high-growth investments or replace a flexible emergency fund — they serve a specific purpose: predictable, locked-in returns for money you won’t need before a known date. Used for the right goal, with a term that matches your actual timeline, a CD can be a genuinely useful, low-risk tool within a broader savings strategy.

This article is for general educational purposes only and does not constitute personalized financial advice. Consult a qualified financial professional for guidance specific to your situation.